Underwriting Heart Disease for Life Insurance

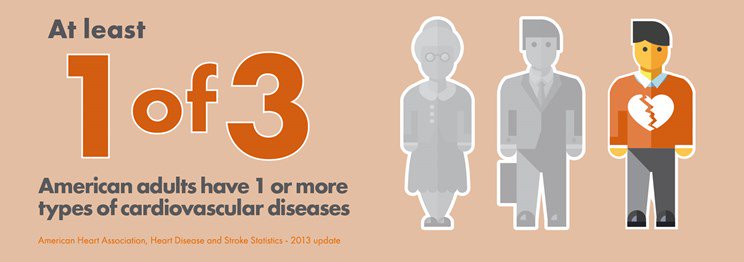

According to the American Heart Association (AHA) Coronary Heart Disease is the leading cause of death in the United States. Approximately 1 of every 3 deaths is caused by cardiovascular disease, which amounts to more deaths than all forms of cancer and chronic lower respiratory disease combined.

Obtaining life insurance for clients with heart disease can often be a complex process because of all the possible factors to be considered. Many people believe that heart disease will disqualify them from getting coverage, however, many Americans can still receive adequate and affordable life insurance.

In order to determine the insurability of a client who discloses a history of heart disease, it is helpful to know which of the subtypes the client is referring to.

Types of cardiac conditions (disease) include:

Vascular: Pertains to the vessels of the heart, usually vessels laden with plaques, which can cause ruptures, and the subsequent obstructions to blood flow. Examples of vascular conditions include: Atherosclerosis, Peripheral Artery Disease (PAD), Carotid Artery Disease (CAD) and Heart Attacks also known as Myocardial Infarction or MI.

Valvular: Defect(s) or damage involving one or more of the four heart valves, which can lead to problems opening and closing of the valve, and/or with creating a proper seal for a heart chamber. Examples of valvular conditions include: Valvular Stenosis, Pulmonic Stenosis, Mitral Stenosis, and Valvular Insufficiency.

Muscular: Inhibits the normal muscular contractions and relaxations of the heart muscle. Examples of muscular heart conditions include: Hypertrophic Cardiomyopathy, Dilated Cardiomyopathy, and Restrictive Cardiomyopathy

Electrical: Interferes with the proper electrical conductivity of the heart, including abnormal heart rhythms and variations in electrical stimulation. Examples include: Arrhythmia, Atrial Fibrillation (AF), Atrial Flutter (AFL), Ventricular Tachycardia (VT), and Long QT Syndrome (LQTS).

Structural: Defective or dysfunctional structure of the heart, often compromised of injured, enlarged, atrophied, or distended chamber, wall, lining, ostium, or septum. Common conditions include: Congenital Heart Disease (CHD), Atrial Septal Defect (ASD), Patent Foramen Ovale (PFO), and Ventricular Septal Defect (VSD).

These conditions are more difficult to quick quote, and may require an underwriting review of full electrocardiogram (ECG) tracings as well as additional tests.

At GBS, heart disease history can be reviewed and unraveled, and preliminary cardiac risk assessments can be pursued from multiple companies. In many cases, this will reveal the most favorable opportunities for meeting your client’s objectives.

As advisors, you can get the ball rolling by having your clients complete our GBS Confidential Life Insurance Questionnaire or by asking your client the following questions:

- Age of onset or diagnosis?

- Treatment, surgeries, or any medications?

- Family history of other types of heart disease?

- Frequency of follow-up visits with cardiologist?

- Lifestyle habits such as smoking, exercise, drug use, etc?

- Current weight and diet?

- Has an actual cardiac event occurred, and if so, when?

Each case’s results will vary, and it is important to ask the right questions in order to better assess your client’s insurability. Once preliminary field underwriting is collected, our underwriter can better determine what carriers would best suit your client’s specific standing.

MORE ADVISORS BLOG

GBS News: Product and Underwriting Updates - Week of October 20 - November 2

Allianz's announced their first ever Risk-Class Upgrade Underwriting Program, offering automatic risk-class upgrades, up front, for qualifying clients.

Read More >>

GBS News: Product and Underwriting Updates - Week of October 9 - October 19

Effective October 9, 2023, iPipeline iGO and LifePipe users can easily access ALL underwriting submission paths in the same session with the new SimpliNow Choice platform.

Read More >>