Underwriting Diabetes for Life Insurance

Did you know affordable life insurance coverage is available for most clients? Here’s what advisors need to know.

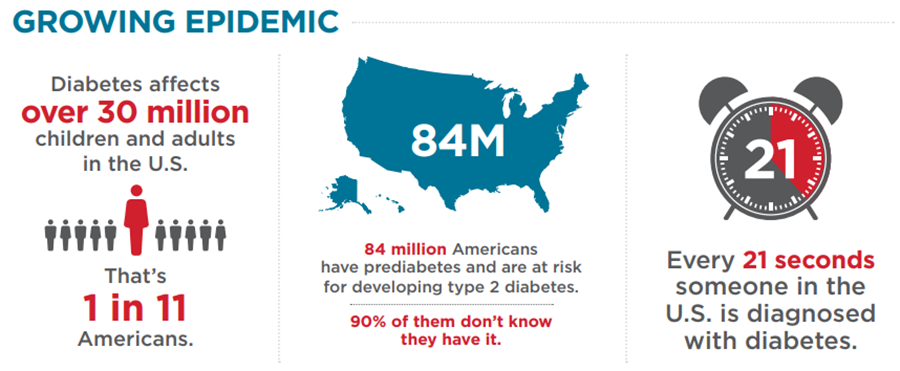

According to the American Diabetes Association, diabetes is the 7th leading cause of death in the U.S. and over 30 million Americans are affected by the condition. The technical term for diabetes is diabetes mellitus (DM) which is a disorder of carbohydrate metabolism. Diabetes affects the body’s ability to process the energy found in food (glucose), which often leads to high blood sugar levels (hyperglycemia) over an extended period of time.

Diabetes mellitus essentially means “a profuse flow of a sweet substance.” The “profuse flow” refers to the excessive urination (polyuria), a classic symptom associated with this disorder. The “sweet substance” included in the excretion is glucose (sugar).

All cells and organisms require energy in order to function. In humans, this energy comes from glucose, a byproduct of the digestion, absorption, and assimilation of food. The glucose is transported by the circulatory system to individual cells, then transported across cellular membranes by insulin, and subsequently converted into energy.

Individuals with diabetes either don’t produce enough insulin, or their bodies are unable to use the insulin it does produce. Common symptoms (in addition to polyuria) associated with diabetes mellitus include sudden weight loss, sudden vision changes, excessive thirst (polydipsia), excessive hunger (polyphagia), labored breathing, lethargy, and a “fruity” breath odor.

The three most common types of diabetes mellitus are as follows:

Type 1 is characterized by inadequate, or highly deficient, or total absence of the production of insulin by the pancreas. It is generally diagnosed earlier in life (for example, from birth to early 30’s). However, it is the lack of insulin that defines the type of diabetes and not the age. This insulin deprivation severely compromises or wholly negates the “insulin transport mechanism,” leaving the cells “gasping” for energy. If not treated, this results in cellular dysfunction and eventually cellular death. Only about 10% of diebetics are considered to have Type 1 diabetes.

Type 2 formerly known as adult-onset diabetes is characterized as an inefficiency in the utilization of insulin. It is usually diagnosed later in life (usually after age 30, but this is not strictly the rule). With Type 2, there is insulin available because at least some insulin is produced by the pancreas (although not always at adequate or optimal levels for some individuals). Essentially, the “transport” function is compromised, preventing glucose from being fully absorbed by the cells – this is called insulin resistance. When cells do not receive sufficient glucose, the pancreas will create more insulin in order to aid the transmission of glucose to the cells. This overproduction of insulin is not sustainable, and eventually causes sugars to build up in the bloodstream. Almost 90% of diabetics suffer from the Type 2 variety.

Gestational diabetes is initially diagnosed during pregnancy for some women. In those instances, placental hormones negatively impact insulin hormone function and lead to higher than normal blood glucose levels. Gestational diabetes might be a precursor to type 1 or type 2 diabetes, but for most women there are no further indications of diabetes post-partum.

There are multiple other types of diabetes mellitus in addition to these three, but they are much less common and are usually secondary to other medical conditions.

Diabetes is considered to be a very significant medical condition. When not properly treated, it is often a precursor to many other medical impairments, many of which can be fatal. These include:

- Coronary artery disease (including heart attacks)

- Peripheral vascular disease (including claudication)

- Cerebrovascular disease (including strokes)

- Hypertensive vascular disease

- Renal failure (including a need for dialysis or kidney transplantation)

- Vision loss (including blindness)

- Nerve damage (including numbness, tingling, and pain)

- Foot problems (including dryness, callouses, ulcers, gangrene, and amputation)

- Hearing loss

- Dementia (including Alzheimer’s disease)

- Stomach problems (delayed gastric emptying)

There are multiple ways to address this condition to mitigate its severity and future complications. These include:

- Dietary changes

- Enhanced exercise regimens

- Weight loss programs

- Lifestyle changes

- Pharmaceutical medications

- Insulin administration

Control of diabetes is largely determined by a blood test commonly called “glycohemoglobin A1c,” or simply “A1c.” In general, there is a direct correlation between higher A1c levels and higher substandard risks assessments.

Underwriting Diabetes

Underwriters will review the following aspects of this condition in making their risk assessments:

- Type of diabetes: type 1, type 2, gestational or other.

- Age at onset – when was it first diagnosed?

- Client’s current age, height and weight.

- Is it well controlled – A1c test is very helpful to know.

- Any complications associated with the condition.

- Type of treatment - diet, oral medication and dosages, insulin shots or pump.

Excellent long-term control of diabetes by individuals currently over the age of 60, not having any documented diabetic complications, might very infrequently be assessed as Preferred. However, most companies usually do not tender an offer better than Standard or Standard Plus for this medical condition. Conversely, individuals with significant diabetic complications might be offered a high substandard rating, or might be uninsurable.

Helpful Links

American Diabetes Association, Statistics About Diabetes.

Infographic, The Staggering Costs of Diabetes.

For additional information, CDC National Diabetes Statistics Report, 2017.

MORE ADVISORS BLOG

GBS News: Product and Underwriting Updates - Week of October 20 - November 2

Allianz's announced their first ever Risk-Class Upgrade Underwriting Program, offering automatic risk-class upgrades, up front, for qualifying clients.

Read More >>

GBS News: Product and Underwriting Updates - Week of October 9 - October 19

Effective October 9, 2023, iPipeline iGO and LifePipe users can easily access ALL underwriting submission paths in the same session with the new SimpliNow Choice platform.

Read More >>