Stable Returns with the Single Premium Life Strategy

By Gregg Kaufman, CLU, CFP

Many of today’s conservative investors and savers are looking for higher rates of return than can be provided by passbook savings accounts and CDs, and are likely to avoid equities because of the downside risk. Annuities are one option, but long surrender periods and lack of early liquidity as well as the lack of guaranteed rates of return might be negatives for some.

Let’s look at Single-Premium Life insurance and compare the advantages and disadvantages to other options that are available to clients with $100,000 to $1,000,000 in liquid assets who might want to reposition funds for higher or more stable rates of return. Clients considering this type of plan must also have a real need for additional life insurance and be insurable.

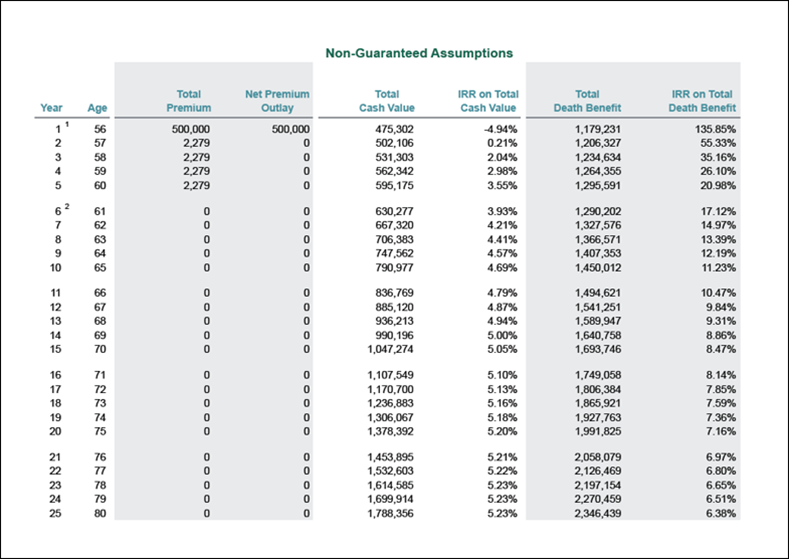

In this example, we’ll put a $500,000 one-time deposit into a dividend paying (participating) whole life contract and solve for the minimum amount of life coverage possible. The death benefit shown is $1,179,231 by the end of the first year and the total cash value available is $475,302 – these numbers assume that the current dividend scale continues all years.

Note that the contract is cash-flow positive after the second year - with the cash surrender value already exceeding the $500,000 premium. By the 10th year, the projected cash is over $790,000 with an IRR of 4.69%. By the 15th year, the client has already doubled their cash value, to over $1,000,000 and an IRR of 5.05%. The illustration below assumes the current dividend scale continues. We suggest showing alternate, reduced-scale illustrations also. (This example shows $500,000 as the “net premium outlay” or the total out of pocket from the client, whereas the $2,279 is taken out of policy values – not from the client.)

Why Whole Life?

Whole Life, as you may know, offers multiple ways to grow cash value. There is a guaranteed minimum cash value, usually set to “endow” at age 100. Plus, there are dividends, i.e., participation in the company’s profits. Lastly, dividends paid annually are usually set to purchase additional incremental amounts of insurance (paid up additions) and this extra insurance also participates in dividends. Virtually all of the well-established mutual whole life carriers can state that they have never missed a dividend, some in over 100 even 150 years!

This concept can be illustrated with any cash value product – we can also supply IUL, UL or VUL proposals, which may project even higher cash values, though the whole life will generally have the strongest guaranteed cash values.

Any single-pay design such as this generally results in a Modified Endowment Contract or MEC, meaning any cash coming out of the contract will be taxed like an annuity, each payment being partly taxable and non-taxable (unless the premium is coming via a 1035 tax-free exchange). The Single Premium Life design still has some advantages over bank accounts and other investments by offering tax-deferred growth. Your interest grows and compounds without being subject to annual income taxation, which would otherwise reduce the total growth.

Benefits of Whole Life for Cash Growth

- Avoids Negative Market Returns

- Tax-Deferred Growth of Cash

- Compounding Growth due to Dividends and Paid-up Additions

- 100+ year history of Dividend Payments

- A+ rated financial institutions

Benefits of Using Life Insurance

- Income Tax-Free Death Benefit

- Early Liquidity and No Early Surrender Charges

- Avoids Probate

- Additional Liquidity via Chronic Illness Rider or Terminal Illness Rider.

- Competitive Internal Rate of Return (IRR)

Who is a Good Candidate?

- Clients must be healthy enough to qualify for insurance.

- Clients must have a need for some additional life insurance.

- Clients should have $100,000 to $1,000,000 in liquid cash, available to reposition and set aside.

- Clients looking for stable, conservative returns.

- Does not need immediate liquidity. This is a moderate to long term strategy

If you have clients looking for a competitive, stable rate of return and could benefit from additional life insurance, please call us for a proposal today.

MORE ADVISORS BLOG

GBS News: Product and Underwriting Updates - Week of October 20 - November 2

Allianz's announced their first ever Risk-Class Upgrade Underwriting Program, offering automatic risk-class upgrades, up front, for qualifying clients.

Read More >>

GBS News: Product and Underwriting Updates - Week of October 9 - October 19

Effective October 9, 2023, iPipeline iGO and LifePipe users can easily access ALL underwriting submission paths in the same session with the new SimpliNow Choice platform.

Read More >>