Introducing the Latest Generation of Asset-Based LTC Plans

By: Gregg Kaufman, CLU, CFP

Asset-Based LTC plans continue to gain popularity in the marketplace while traditional plans are declining both in sales and number of carriers offering them. Here is a quick introduction to some of the features and benefits of these plans. Though the upfront costs may be higher, the availability of rate guarantees, cash value and other benefits make them a more attractive choice than ever before. Traditional plans are still available and offer the lowest cost in many cases. Many financial advisors are presenting these products as a way to reposition cash assets into leveraged protection assets, with risking little or no principal.

Features available in some Asset-Based Plans:

- Rate guarantee on most plans.

- Can offer life-time benefit plans instead of just 4-5 year plans.

- Life insurance benefits over and above the premium paid.

- Other funding options such as Annual-Pay or Ten-Pay available in some plans.

- Includes cash value or return of some premium if client quits plan.

- May cover two lives as a shared or pooled benefit.

- Underwriting is usually more liberal, exams rarely required.

- Some can be funded with Qualified Plan money.

- Can be funded with life insurance or annuity roll-overs.

- Pension Protection Act rollovers can shield clients' taxable gains in highly appreciated annuities.

- Some tax deductibility may be available for businesses, especially C-Corps.

Live, Quit or Die

Whereas traditional LTC plans run the risk of the client never getting any benefits from the plan if they don't file a claim, the new Asset-Based contracts offer the so-called live, quit or die proposition, meaning that the client will receive a sizable benefit back one way or another.

- Live long enough to go on claim and receive the intended long term care benefits back.

- Quit the plan and receive the surrender value which might equal or exceed the premium paid.

- Die and receive a death benefit in excess of the premium paid (available on many plans.)

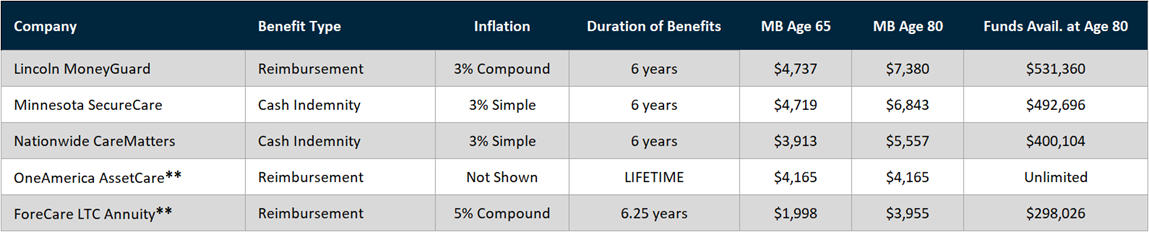

In the comparison below, we look at five popular Asset-Based plans to examine how well they leverage a client’s assets by creating a large pool of funds available to provide for LTC claims.

Five Popular Asset-Based Plans Compared

- Male, Age 65.

- Each plan started with a one-time $100,000 deposit.

- Not all products available in all states.

- MB = Monthly Benefit.

Each product listed started with a single deposit of $100,000 on a male, 65 to compare the relative leverage and benefits of each. The last option is an LTC annuity. The last two actually offer a choice between individual coverage or joint life coverage, so benefits for a couple are shown in this example.

**JOINT POLICY COVERING TWO INSUREDS AVAILABLE

Benefit Type – Cash Reimbursement vs Full Indemnity

- Cash reimbursement plans are the most commonly available type of plan, where the insurer will reimburse claims only after reviewing receipts showing an actual expense for long term care were incurred.

- A full indemnity benefit may be more expensive but can pay the entire monthly benefit to the client regardless of expenses or claim size, up to policy limits.

You can see from the above comparison that $100,000 can be leveraged into 300% percent to over 500% or more, and one plan offers unlimited lifetime benefits. (Less leverage is available at older issue ages.) Virtually all of the above plans offer a guaranteed premium, a surrender value and benefits of 6-years or more. The newest generation of Asset-Based plans offer some form of streamlined underwriting, with no exam in most cases.

When the earliest Asset-Based products first came to market over 20 years ago, they were traditionally funded with a single-premium. Now we have various funding options available such as 10-pay, 20-pay, and other durations, even level pay in some cases. The single-pay design is useful for 1035 rollovers from life policies and annuities. In addition, qualified-plan rollovers can be used to fund specialized products.

Annuity Rollovers and the Pension Protection Act Funding

Another funding option that can be used with some of these plans involves taking advantage of the Pension Protection Act of 2006, which states that a client with a high appreciated annuity can roll that value over into a plan providing long term care benefits and escape the capital gains completely if all values are used for LTC coverage and benefits. So in addition to the leverage shown above, an additional tax advantage is available to clients looking to fund care coverage with an Asset-Based plan. Click here to find out more about the Pension Protection Act.

There is a large variety of plans and funding vehicles available in this area, more than can be covered in a short article such as this. Please contact your marketing representative to discuss your specific client's details and options.

MORE ADVISORS BLOG

Webinar Invitation: How to Position LTC as a Retirement Planning Tool

Join us for a special webinar featuring Mutual of Omaha discussing how agents can position LTC as a retirement planning tool. We will be going over today's LTC changing market with real world statistics, how to start the conversation, tax favorability and more.

Read More >>GBS News: WA State LTC Update | DI Sales Opportunities | Fixed Index Annuity | and more

The soon-to-be-enacted "Long Term Services and Trust Act" will impose a .58% annual tax on Washington state's workforce to fund one year of future LTC benefits (non-portable and only available if still living in WA). The only way to "opt-out" and avoid paying this tax is to show proof of existing coverage.

While the Trust Act could be beneficial for low-to-middle income earners, it negatively impacts those highly compensated individuals who will pay a much larger, disproportionate amount for the same, minimal benefit.

Read More >>